7 Things Queensland Agents Should Know About the New Forms Live Contracts

With Forms Live relaunching directly in the Sunshine State, agents now have a genuine choice of contract platform for the first time in over a decade.

9 min read

Understand the difference between CDD and VoI under Australia’s Tranche 2 AML reforms. What real estate agents and conveyancers must do before July 2026.

As Australia's Tranche 2 AML reforms approach, one of the most common questions from real estate agents and conveyancers is: "Isn't this just VoI?"

It's a fair question. Verification of Identity (VoI) has been part of property transactions for years. Most agencies already have processes in place to confirm a client's identity before settlement. But the short answer is no. AML compliance under Tranche 2 is not simply VOI under a different name.

Customer Due Diligence (CDD), as required under Australia's Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) reforms, introduces a broader, deeper and ongoing obligation. Understanding the distinction between CDD and VoI is one of the most critical things property professionals can do before 1 July 2026.

This is not a minor procedural update. It represents a fundamental shift from identity verification to risk-based compliance.

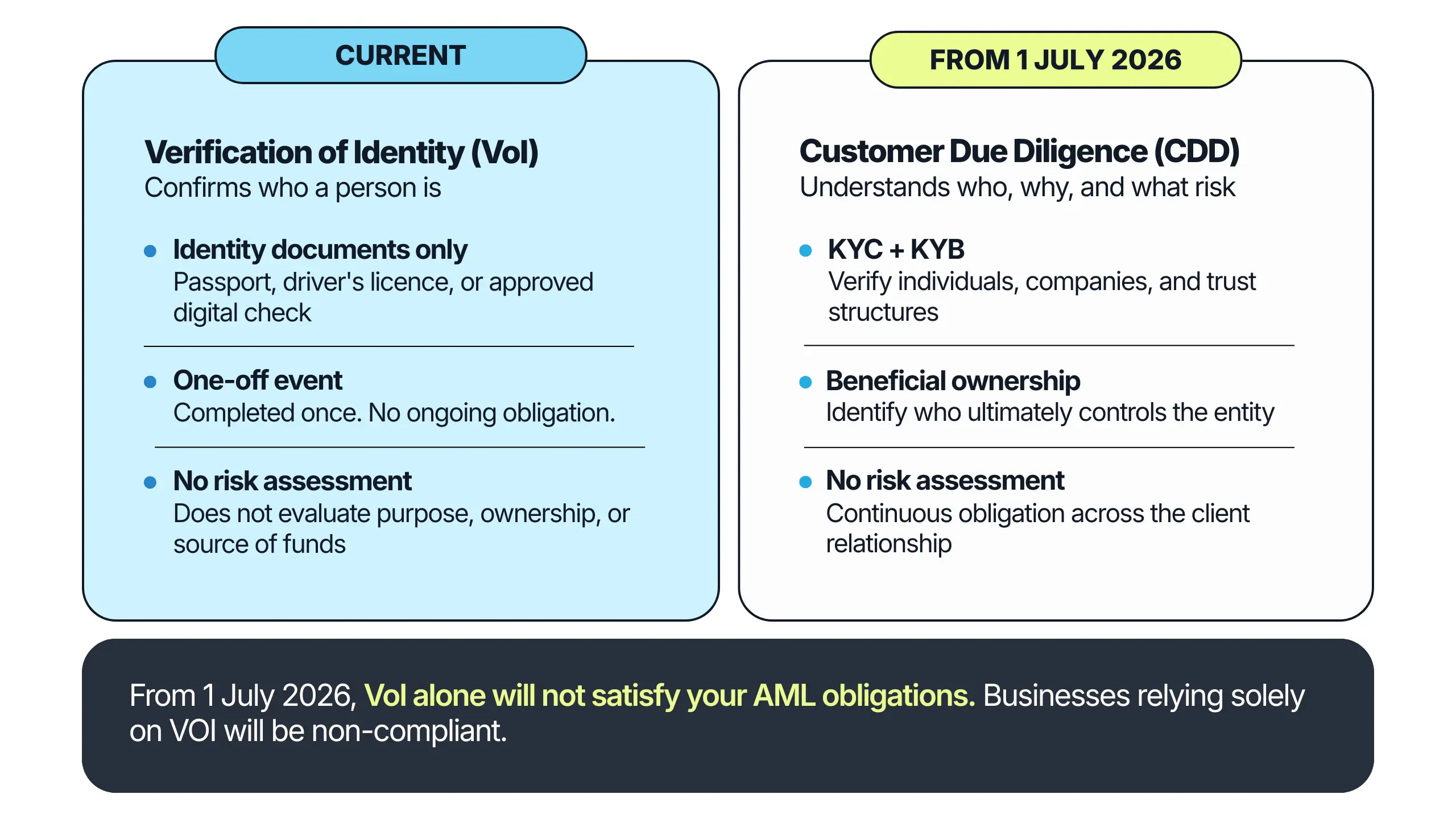

VoI is a familiar concept within the property industry. It confirms that a person presenting for a land or property transaction is who they claim to be.

In practice, VoI involves reviewing identification documents such as passports or driver's licences, conducting in-person or approved digital identity checks, and ensuring compliance with state-based land title requirements. Once identity has been confirmed according to prescribed standards, the VoI process is complete.

The process of VoI is transactional and event based. It exists to protect the integrity of land transfers and reduce identity fraud. It answers a single question: Is this person who they say they are?

Under the current system, once that question is satisfied, the obligation ends.

CDD is fundamentally different to VoI.

CDD is the broader compliance framework required under Australia's AML/CTF obligations and will apply to real estate agents and conveyancers from 1 July 2026 under Tranche 2 reforms. Rather than focusing solely on identity, CDD requires businesses to understand the customer, the transaction, the ownership structure, and the associated risk.

CDD includes the following components:

In plain terms: VoI verifies identity. CDD evaluates identity, ownership, intent, and risk.

Under Tranche 2 reforms, property professionals will be required to conduct CDD before providing designated services. This includes identifying beneficial ownership, assessing and documenting risk, maintaining detailed records, and reporting suspicious matters to AUSTRAC within prescribed timeframes.

While VoI may form part of the KYC component of CDD, it is only one element of a much broader framework.

Relying solely on VoI will leave your business non-compliant because it does not address:

The regulator's focus is not limited to confirming identity. AUSTRAC is concerned with preventing the misuse of property transactions for money laundering, terrorism financing, and proliferation financing. The difference between VoI and CDD is not administrative. It is structural.

Consider a scenario where a company purchases a residential property through one of its directors.

Under existing processes, VoI may confirm the director's identity. The agency verifies their driver's licence, confirms their details, and proceeds with the transaction.

Under AML/CTF obligations, this is insufficient.

CDD would require the agency to:

Without this broader understanding, the agency risks failing its AML obligations, even if VOI was performed correctly.

From 1 July 2026, real estate agents and conveyancers will be subject to formal reporting obligations under Australia's AML/CTF reforms. These include:

These obligations reinforce why structured CDD processes matter. Risk assessments, client profiles, and transaction monitoring must be documented and retrievable. The emphasis is not only on compliance. It is on the ability to demonstrate compliance if audited or reviewed.

For many agencies, the biggest challenge is operational rather than conceptual. Understanding CDD is one thing. Implementing it consistently without disrupting client experience is another.

The key questions agencies need to answer are:

Integrated AML software plays a critical role here. Platforms such as APLYiD, easyAML, AMLHUB, and First AML provide dedicated AML compliance tools tailored to Australian businesses, including automated CDD, beneficial ownership identification, sanctions and PEP screening, and ongoing monitoring. These systems centralise documentation and provide governance oversight dashboards that give principals and compliance officers real-time visibility.

When integrated with workflow solutions like Forms Live, CDD can be embedded directly into client onboarding processes. Identity verification, risk profiling, and compliance tracking become part of the client intake workflow rather than a separate manual task. This reduces friction, improves consistency, and supports role-based accountability across the business.

From 1 July 2026, real estate agents and conveyancers will be fully subject to Australia's AML/CTF reforms under Tranche 2.

VoI remains relevant, but it is only one component of the new compliance framework. AUSTRAC's objective is to strengthen transparency and protect the integrity of Australia's property market. Agencies that understand the distinction between VoI and CDD early will be better positioned to implement structured, audit-ready systems well before enforcement begins.

Preparation now allows your business to move from uncertainty to clarity, and from reactive compliance to proactive risk management.

Not sure how your current VoI processes stack up against Tranche 2 CDD requirements? Our free AML Essentials Checklist breaks down what's required step by step, so you can identify gaps and get ahead of the deadline.

Download the Free AML Essentials Checklist →

What is the difference between CDD and VoI? VoI (Verification of Identity) confirms that a person is who they claim to be, using approved identification documents. CDD (Customer Due Diligence) goes significantly further. It verifies identity, identifies beneficial owners, assesses risk, understands the purpose and nature of the transaction, and requires ongoing monitoring throughout the client relationship. From 1 July 2026, VoI alone will not satisfy AML obligations under Tranche 2.

Do real estate agents need to register with AUSTRAC under Tranche 2? Yes. From 1 July 2026, businesses providing designated real estate services must enrol with AUSTRAC and comply with AML/CTF obligations. Enrolment opened 31 March 2026.

What is a Beneficial Owner in real estate AML compliance? A beneficial owner is the individual who ultimately owns or controls an entity involved in a property transaction. Under Tranche 2 CDD requirements, agencies must identify the beneficial owner even where transactions are conducted through companies, trusts, or other structures, not just the person presenting for the transaction.

What is Enhanced Due Diligence (EDD)? EDD is a higher level of scrutiny applied when a client or transaction presents an elevated risk. This might include complex ownership structures, clients from high-risk jurisdictions, or transactions that are inconsistent with a client's known profile. Agencies must have processes in place to identify when EDD is required and document the additional steps taken.

What are the reporting deadlines for SMRs under Tranche 2? Suspicious Matter Reports (SMRs) must be lodged with AUSTRAC within three business days of forming a suspicion. If terrorism financing is suspected, this timeframe reduces to 24 hours.

Is CDD required for every property transaction? CDD is required before providing designated services. Standard CDD applies to most client relationships, but the level of due diligence required varies based on risk. Higher-risk clients or transactions may require Enhanced Due Diligence (EDD), while lower-risk situations may be managed with Simplified Due Diligence (SDD), though AUSTRAC has not yet confirmed the full scope of SDD provisions for the real estate sector.

Not sure where to start? We've put together a practical AML Essentials Checklist to help real estate agents and conveyancers track their compliance preparation step by step.

Download the Free AML Essentials Checklist →

The Forms Live platform is the leading provider of forms and contracts for the real estate industry around Australia and is owned by Dynamic Methods. It is used by 8,500 real estate agencies and more than 50,000 agents and managers. More than 60 million of our forms have been used since launch in 2005 resulting in more than $100m in property sales per month and a further $80m in property leases per month.

With Forms Live relaunching directly in the Sunshine State, agents now have a genuine choice of contract platform for the first time in over a decade.

9 min read

The Forms Live integration with APLYiD means the step from data capture to full due diligence is a short one. Here's what that looks like in practice, and why it matters.

4 min read

Do real estate agencies need AML software under Tranche 2? Learn how Australian property businesses can meet AUSTRAC compliance requirements before July 2026.

9 min read